Complete Guide to Home Mortgages for Beginners 2026: Requirements, Process & Bank Approval Tips

Writing & Research Team

First time applying for a mortgage? This complete 2026 guide covers everything — eligibility requirements, step-by-step application process, interest rate types, and proven tips to get your home loan approved by the bank.

The Complete Guide to Home Loans for First-Time Buyers 2026: Requirements, Process, and Tips to Get Approved

Buying a home is one of the biggest financial decisions you will ever make. Yet for many people, particularly young adults who are just starting their careers, rising property prices can feel like a gap that only widens over time. This is where a home mortgage, known in Indonesia as KPR (Kredit Pemilikan Rumah), becomes the most realistic solution: it lets you own a home without waiting a decade or more for your savings to catch up.

The government has been actively supporting homeownership through the 3 Million Homes program, backed by regulatory frameworks from the Financial Services Authority (OJK) and Bank Indonesia to encourage national banks to extend more property financing. In practical terms, the opportunity to secure a home loan in 2026 is more accessible than it has been in previous years, provided you understand how the process actually works.

This guide is written specifically for those considering a home loan for the first time. It covers how mortgages work, what requirements you need to meet, what documents to prepare, and the concrete steps that give your application the best chance of approval.

A. What Is a Home Loan and How Does It Work?

Simply put, a home loan is a bank facility used to purchase residential property, whether a landed house, apartment, or shophouse. You pay a portion of the purchase price upfront as a down payment (DP), while the bank finances the remainder. From there, you repay the loan in monthly installments over an agreed period, plus interest.

Think of it like renting, except every payment you make is gradually building ownership of a real asset, not disappearing into someone else's pocket.

Key Components of a Home Loan

Before going further, get familiar with the basic terms that will appear throughout the entire loan process:

Credit ceiling (plafon) — the total amount the bank will lend, calculated as the property price minus your down payment.

Down payment (DP) — the portion of the purchase price you pay directly at the start of the transaction. The amount varies, typically starting from 10-20% depending on the bank's policy and loan type.

Tenor — the loan repayment period, usually between 5 and 30 years.

Interest rate — the cost of borrowing, which can be fixed or floating.

Monthly instalment — the amount you pay each month, consisting of principal repayment plus interest.

Subsidised vs. Non-Subsidised Home Loans: Which One Is Right for You?

In Indonesia, there are two main types of home loans. The first is the subsidised home loan through the FLPP scheme (Fasilitas Likuiditas Pembiayaan Perumahan), a government programme offering a fixed interest rate of 5% per year for a tenor of up to 20 years, exclusively for low-income households. There is no floating rate adjustment, which means your monthly instalment stays the same for the entire loan period.

The second is the non-subsidised or commercial home loan, which uses market interest rates and is available to all income segments. The rate is competitive at the start during the fixed-rate period, but it will shift in line with Bank Indonesia's benchmark rate once the promotional period ends. This type of loan offers a much wider selection of properties, with no ceiling on purchase price.

B. Home Loan Requirements for 2026

General Eligibility Criteria

Banks apply a set of baseline requirements before accepting any application. Applicants must be Indonesian citizens and at least 21 years of age, or already married even if they have not yet reached that age.

What many people overlook is that the age limit applies to when the loan is fully repaid, not when it is applied for. Most banks set the maximum age at 65 for employees and 70 for self-employed borrowers. This means a 45-year-old applicant can only take a maximum tenor of 20 years, not 30 and as a result, the monthly instalment will be higher.

On the employment side, salaried employees should ideally hold permanent status with at least two years of service. Self-employed individuals can also apply, as long as their business has been running for at least two years and they can demonstrate stable income through proper financial records.

Financial Requirements: Understanding the Debt Service Ratio (DSR)

A bank will not approve a loan that places excessive strain on your finances. The principle used is the Debt Service Ratio (DSR), the proportion of your total monthly loan obligations relative to your net income. The safe threshold is generally a maximum of 30-40% of income.

In practice, if your net monthly income is IDR 10 million, the maximum monthly instalment a bank will approve is around IDR 3-4 million. If you already have other active instalments, a motorcycle loan or credit card debt, for instance, those are counted together in the same calculation. The implication is clear: reduce or settle existing debts before submitting a home loan application.

Credit History and the OJK Financial Information System (SLIK)

One of the most common reasons for rejection is a poor credit history. Banks will check your credit profile through the Financial Information System (SLIK) managed by OJK. This system records every borrowing history tied to your identity, online loans, credit cards, vehicle financing, and more.

The ideal credit status is collectability 1 (Current), meaning no arrears on any loan. It is worth noting that OJK has officially stated there is no regulation that categorically prohibits issuing a home loan to borrowers with a non-current credit history. However, the final decision rests with each individual bank based on its own risk management policies. In practice, the cleaner your credit record, the stronger your application.

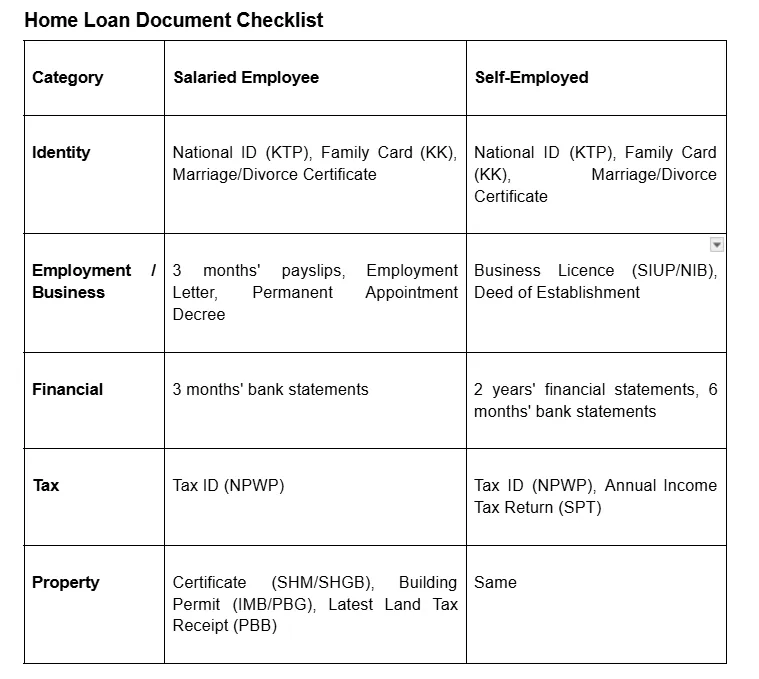

Documents You Need to Prepare

Many home loan applications stall not because of credit issues, but because of incomplete or mismatched documents. Have everything ready before you approach the bank — not after.

For salaried employees specifically, some banks will also require a copy of the Permanent Appointment Decree as formal proof of permanent employment status, a general employment letter alone may not suffice. Make sure this document is available before the process begins.

PropertyID Editorial

Our expert writing team is dedicated to providing the most comprehensive, reliable property news and guides in Indonesia.